For nearly two decades, enterprises and their payments partners have turned to the Payment Card Industry Data Security Standards (PCI DSS) for guidelines on how to mitigate payment data risks. These guidelines have evolved with the industry, introducing new requirements to help businesses ward off emerging payment data threats. The latest iteration (PCI DSS 4.0) introduces significant changes that enterprises must adapt.

What is PCI DSS 4.0?

An S&P Global Market Intelligence study commissioned by Bluefin – The State of Enterprise Readiness for PCI DSS 4.0 – looked for insights. Surveying over 250 payment data security professionals at enterprises across nearly a dozen industry verticals, the study prioritized respondents with intimate knowledge of PCI DSS compliance, guidelines, and requirements. The results provide a view into the current state of payment data security and establishes a baseline for PCI DSS 4.0 readiness.

As the report states, “PCI DSS is a set of standards established by the PCI Security Standards Council (SSC) for payment service providers and merchants to protect customer payment data. The PCI SSC formed the first set of standards in 2004, and it put forth the current iteration, PCI DSS 3.0, 10 years ago. While there have been various adjustments to requirements in 3.0, they are smaller and more short-term-focused compared to the overhaul that 4.0 will require. The standards are not required by law or regulatory mandate but self-governed and imposed by the global card networks on merchants, payment processors, service providers and others in the payments ecosystem.”

Key Changes in PCI DSS 4.0

Merchant Risk Council’s article featuring industry expert Dan Fritsche explains that “4.0 has over 50 new requirements, with 13 effective as 4.0 is rolled out, meaning everyone will need to meet those by March 31, 2024 if not sooner. The remaining requirements are listed as best practices and will become requirements as of March 31, 2025, allowing flexibility for an organization to figure out what makes sense for them to implement in what order based on their specific organizational risks.”

The several enhancements and amendments in the newest version include the following:

- Increased security, expanded multi-factor authentication, updated password specifications and updated requirements to address phishing and security breaches.

- New requirements that support payment technology innovation and flexibility to allow different methodologies to achieve security goals. Organizations can use a defined or custom approach to meet requirements.

- Updated guidance on implementing security controls and updated specifications on roles and responsibilities for each updated requirement.

- Inclusion of detailed verification and reporting options to enhance verification methods and procedures.

The best resource for navigating all requirements, Fritsche notes, is the PCI SSC website, which includes a PCI DSS 4.0 Resource Hub.

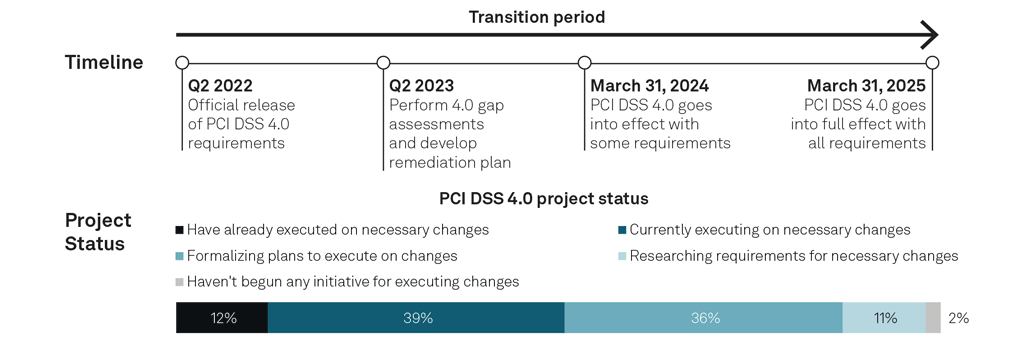

PCI DSS 4.0 Compliance Deadlines

Organizations subject to PCI DSS should understand the key milestones associated with the transition from PCI DSS 3.2.1 to PCI DSS 4.0. While PCI DSS 4.0 was introduced to address evolving security threats and modern payment technologies, compliance requirements were implemented in phases to give organizations time to adapt.

PCI DSS 4.0 Released in March 2022

The PCI Security Standards Council (PCI SSC) officially released PCI DSS 4.0 in March 2022. The updated standard introduced new security requirements, expanded authentication controls and greater flexibility through customized approaches to achieving compliance objectives.

PCI DSS 3.2.1 Retired in March 2024

PCI DSS 3.2.1 remained active during a transition period to allow organizations time to prepare for the new requirements. However, PCI DSS 3.2.1 was officially retired on March 31, 2024, making PCI DSS 4.0 the only active version of the standard.

Future-Dated Requirements Became Mandatory on March 31, 2025

When PCI DSS 4.0 was released, several new requirements were initially designated as best practices to provide organizations with additional implementation time. These future-dated requirements became mandatory on March 31, 2025, marking the final phase of the PCI DSS 4.0 transition.

Organizations that store, process or transmit cardholder data should ensure they have addressed all applicable PCI DSS 4.0 requirements and validated their compliance against the current standard.

How PCI DSS 4.0 Impacts PCI Scope

PCI DSS 4.0 introduces new security requirements and validation expectations, but one principle remains unchanged: the larger your Cardholder Data Environment (CDE), the more systems, controls and processes fall within scope for PCI compliance.

PCI scope includes any people, processes and technologies that store, process or transmit cardholder data, as well as systems that can impact the security of those environments. As organizations expand payment channels and adopt new technologies, maintaining and securing the CDE can become increasingly complex.

More Systems in Scope Means More Compliance Requirements

Every system that stores, processes or transmits primary account numbers (PAN) may be subject to PCI DSS requirements. Connected systems that can affect the security of cardholder data may also fall within scope, increasing compliance obligations, audit complexity and operational costs.

PCI DSS 4.0 Places Greater Emphasis on Security Controls

Expanded requirements around authentication, monitoring, testing and risk management mean organizations must have greater visibility into their payment environments. The larger the CDE, the more challenging it becomes to implement and validate these controls consistently.

Reducing PCI Scope Remains a Best Practice

One of the most effective ways to simplify PCI DSS 4.0 compliance is to reduce where cardholder data exists within the environment. Technologies such as PCI-validated point-to-point encryption (P2PE) and tokenization help minimize the number of systems that handle sensitive payment data, reducing both risk and compliance burden.

By limiting the exposure of cardholder data and shrinking the Cardholder Data Environment, organizations can streamline compliance efforts while strengthening overall payment security

How do Enterprises feel about PCI DSS 4.0?

Enterprises are under pressure to deliver payment experiences that let their customers transact wherever and however they prefer. Diversification of payment channels and methods is expanding the attack surface, attracting growing attention from hackers and fraudsters. This has put payment and risk professionals on high alert.

Enterprises are under pressure to deliver payment experiences that let their customers transact wherever and however they prefer. Diversification of payment channels and methods is expanding the attack surface, attracting growing attention from hackers and fraudsters. This has put payment and risk professionals on high alert.

The S&P Global report shows that payment data security concerns are widespread and significant, with 94% of respondents having significant or very significant concerns pertaining to payment data security, and only 21% saying they are very confident in their ability to protect customer data today.

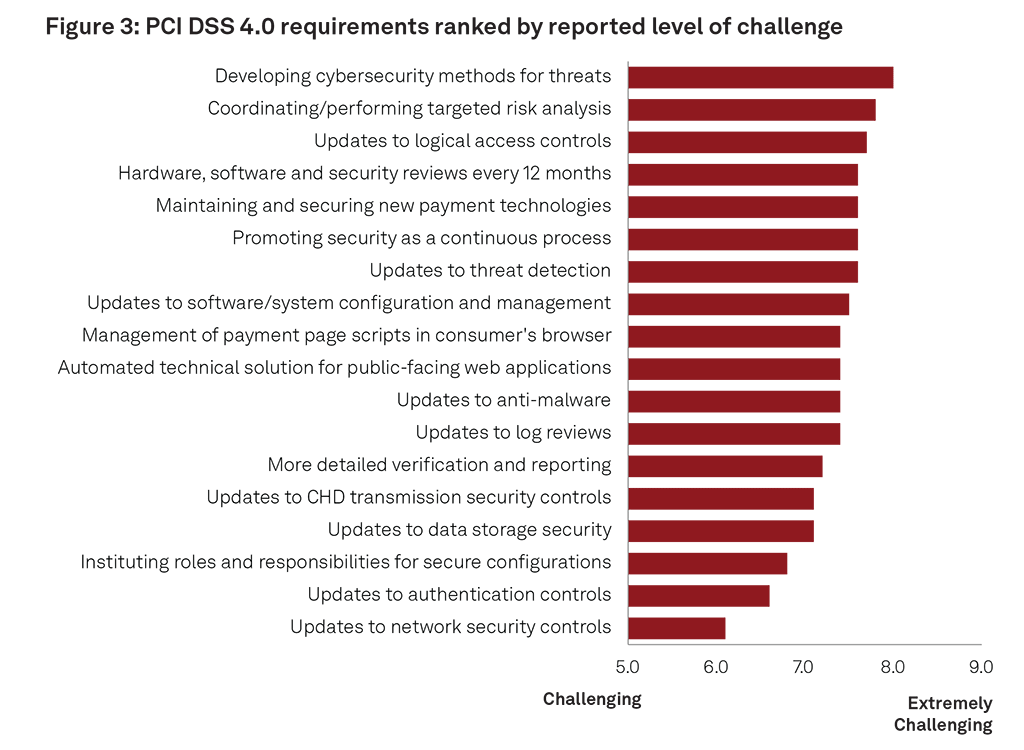

The new list of requirements brought on by PCI DSS 4.0 are designed to combat emerging threats and to ensure the protection of sensitive customer financial data from cyberattacks. The report ranked these requirements by the perceived challenge of implementation, with developing cybersecurity methods for threats topping the list.

The time and resources it will take to complete the requirements is not lost on enterprises.

“PCI DSS 4.0 necessitates a significant lift, and meeting the deadline is a growing concern. Ninety-three percent of respondents indicate the changes required by PCI DSS 4.0 are significant. Further, 90% are concerned about meeting the timeline, and 64% say they would be likely or very likely to accept a timeline extension.” – page 6.

PCI DSS 4.0 vs PCI DSS 3.2.1

| Area | PCI DSS 3.2.1 | PCI DSS 4.0 |

|---|---|---|

| MFA | Limited | Expanded |

| Authentication | Older Controls | Stronger requirements |

| Security Reviews | Less frequent | More continuous validation |

| Flexibility | Prescriptive | Customized approach option |

| Phishing Controls | Limited | Expanded focus |

Simplify PCI DSS 4.0 Compliance with Bluefin

While PCI DSS 4.0 presents an array of operational and resource hurdles for enterprises, there are clear benefits for the enterprise industry. Those that approach it with a strategic mindset stand to differentiate themselves in the marketplace and deliver a superior customer experience.

Technologies such as PCI-validated point-to-point encryption (P2PE) and tokenization help reduce cardholder data exposure, simplify PCI scope and support a stronger security posture under PCI DSS 4.0. By securing payment data at the point of interaction and minimizing the number of systems that handle sensitive information, organizations can reduce risk while making compliance more manageable.

Learn how Bluefin’s PCI-validated P2PE and tokenization solutions can help your organization strengthen payment security and simplify PCI DSS 4.0 compliance.

PCI DSS 4.0 FAQs

Is PCI DSS 4.0 mandatory?

Yes. PCI DSS 4.0 is the current version of the Payment Card Industry Data Security Standard and applies to organizations that store, process or transmit cardholder data. PCI DSS 3.2.1 was retired on March 31, 2024, making PCI DSS 4.0 the active standard for compliance validation.

How Do Organizations Prepare for PCI DSS 4.0?

Organizations should begin by assessing their current PCI environment, identifying gaps between existing controls and PCI DSS 4.0 requirements, and reviewing any future-dated requirements that became mandatory in 2025. Many organizations also strengthen authentication controls, expand multi-factor authentication, improve monitoring processes and reduce PCI scope through technologies such as tokenization and PCI-validated point-to-point encryption (P2PE).

What Is the PCI DSS 4.0 Compliance Deadline?

PCI DSS 4.0 was released in March 2022, and PCI DSS 3.2.1 was officially retired on March 31, 2024. Additional future-dated requirements that were initially considered best practices became mandatory on March 31, 2025. Organizations should now validate compliance against the full PCI DSS 4.0 standard.

Who Must Comply With PCI DSS 4.0?

PCI DSS 4.0 applies to any organization that stores, processes or transmits payment card data. This includes merchants, payment processors, service providers, ecommerce businesses, healthcare organizations, financial institutions and other entities that handle cardholder information as part of their operations.